If I’d been out till quarter to three

Would you lock the door

Will you still need me, will you still feed me

When I’m sixty-four.

– The Beatles

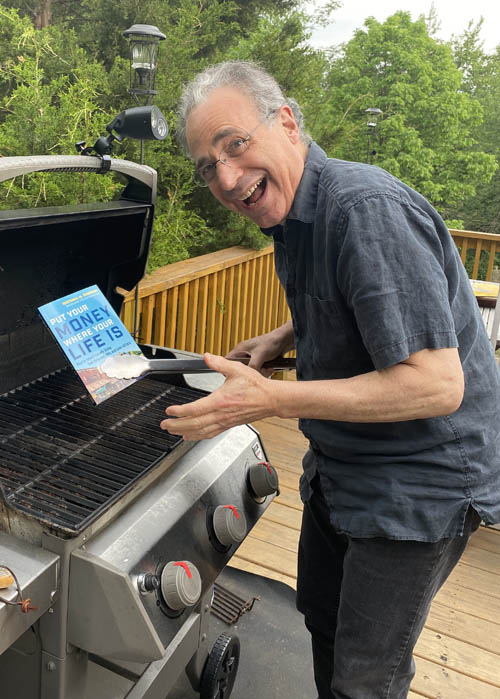

If ever there were an inauspicious week for the release of my latest book, PUT YOUR MONEY WHERE YOUR LIFE IS, this is it. Okay, maybe the week of September 11, 2001, or December 7, 1941. This was also the week I turned 64 on 6/4.

When I was about 6.4 years old, in 1963, my parents took me to Washington, DC, to Martin Luther King Jr.’s “Freedom March,” where he delivered his most famous speech. How far his dream seems today, fifty years later. But we have learned a few things along the way.

When I was half my current age, at 32, I had set up a nonprofit called the Center for Innovative Diplomacy to help mobilize cities in foreign policy. One of the most successful campaigns we participated in was divestment from South Africa. After about half the states and hundreds of cities pulled their investment dollars out of firms doing business in that racist state–joining cities, colleges, and socially responsible investors all over the world–apartheid collapsed. All the skeptics who said shifting a few billion dollars would have no effect were completely wrong.

Where we put our money matters. And that lesson, I believe, highlights what’s gone wrong in America’s communities. If all of us invest in global companies–as we have done for the last 50 years and are doing today–the local businesses that are the foundation of our communities will necessarily atrophy. If you invest in “gazelles” promising 20x returns, the entrepreneur you’ve overlooked who is building a grocery store in the food desert in our backyard will certainly fail. If we don’t shift our investing patterns in the coming months, millions of critically important local businesses may declare bankruptcy.

Part of the story of inequality in America is our systematic underinvestment in communities of color and the essential local businesses needed to serve them. Before the COVID-19 crisis, U.S. households held $56 trillion in long-term investments in stocks, bonds, mutual funds, pension funds, and insurance funds. Even though local businesses account for 60-80% of the U.S. economy, hardly a penny of this $56 trillion touched any local businesses whatsoever. This represents a colossal capital market failure, and investment choices that are inevitably strangling communities across America.

If we fixed our investment system, if we moved 60% of $56 trillion from Wall Street to Main Street, every community would enjoy about $100,000 of additional capital per resident. A small town of 10,000 people would have $1 billion to put into reviving its small businesses post-COVID. A modest city of 100,000 would have $10 billion, enough to reverse the decades of disinvestment that were triggered by foolish “free trade” agreements. And if we focus this capital on the neighborhoods in poverty, we would have a shot at giving tens of millions of Americans renewed opportunities and hope.

There’s no easy solution to our nation’s problems. But I’m absolutely certain that if each of us with retirement savings commits to putting something into community renewal – 10%, 5%, even just 1% – we can shift the course of history.

Here’s one hopeful factoid: Since 2016, federal crowdfunding has been legal. Tens of thousands of Americans have put nearly half a billion dollars into local and small businesses. As my friends Amy Cortese and Arno Hesse have shown, the biggest beneficiaries have been female and nonwhite entrepreneurs—exactly those people the current capital system leaves behind.

If we want economic justice, then we should invest in the people, projects, and businesses that can achieve it.

I could be handy, mending a fuse

When your lights have gone

You can knit a sweater by the fireside

Sunday mornings go for a ride

Doing the garden, digging the weeds

Who could ask for more?

Will you still need me, will you still feed me

When I’m 64.

PUT YOUR MONEY WHERE YOUR LIFE IS shows you exactly how you can reinvest your tax-deferred pension savings and put them to work in your community. You can use your money to get yourself or your kids out of debt. You can help neighbors become homeowners. You can support local businesses, of course, and you can investment in community investment funds.

If you’re interested in learning more, I’ve posted an excerpt from the book that will give you a taste of what’s possible. Please click here, download, and read.

Better still, buy a copy of the book–I can’t imagine a better birthday gift! My publisher, Berrett-Koehler has agreed to give you a discount of 30% if you order by next Monday. Just go here.